Since 2013, LED companies have been full of orders, product output has increased, sales have increased at the same time, enterprises are fully loaded or overloaded, and capacity utilization has gradually increased. LED Lighting products have become the development direction of the next generation of new light sources. The products have been further promoted through demonstration applications, and the energy saving and emission reduction effects are increasingly significant. How will the LED industry develop in 2014? We analyze and predict the trend of industrial development from the aspects of upper, middle, lower reaches and equipment.

Upstream: the price war gradually turns into a technical war

The LED chip industry will not increase production, and sapphire will continue to increase prices, so the chip does not have much room for price cuts.

To say that 2013 began with price wars and mergers and acquisitions, after 2014, the upstream of the LED industry will gradually turn to technical warfare and patent warfare. In 2013, the LED chip industry is already in a state of increasing production and not increasing revenue, and sapphire will continue to increase prices, so the chip does not have much room for price cuts. If there is no technological breakthrough, the price cuts will slow down in the next two years.

After the merger, integration and expansion of major companies in 2013, domestic chip companies have already had large-scale production capacity. At the same time, the patent issue has also begun to emerge. Companies have bolstered the risks posed by patents by strengthening technology research and development, establishing patent pools and other means. In 2013, LightaCorporaTIon, a wholly-owned subsidiary of Sanan Optoelectronics, acquired a 100% stake in Luminus Devices, Inc. (hereinafter referred to as US Lumen) for US$22 million. U.S. lumens has 151 patents covering the entire world of LED chips, packaging, systems and applications. The company's main high-power chips are dedicated to the development of large-area, high-efficiency LED chips. The acquisition of US lumens will greatly enhance the technical strength of Sanan Optoelectronics on the power chip, and also solve some patent problems, opening a window for its international development.

Midstream: Lighting market growth drives package scale

Packaging companies that are squeezed by both upstream and downstream will use large-scale production to ease the pressure of survival through joint and merger methods.

In 2013, the global LED lighting market grew rapidly. According to statistics, the output value of LEDs for lighting applications reached US$3.7 billion in 2013, accounting for 29% of the total LED package output. It is estimated that the proportion of lighting in the overall package will reach 33% in 2014, making it the highest category among all LED applications. In 2014, global LED lighting products shipments are expected to increase by 68%, with an output value of US$17.8 billion. Affected by the demand for LED lighting, the output value of many packaging companies in 2013 exceeded the highest level in history. At a time when the penetration rate of the backlight market is becoming saturated, how to grasp the opportunities of rapid development of the global lighting market will be an important factor in determining the success or failure of the enterprise.

At present, the epitaxial wafer is gradually transitioning from 2 inches to 4 inches, and the cost of the chip is gradually decreasing. If this technology is mature, the price of the chip will still have room to fall in the next few years, so the upstream enterprises are forced to engage in technological breakthrough work. When the technology reaches the bottleneck, it can only compress the chain of the industry chain. Chip companies began to extend to the package, and some chip manufacturers even began to manufacture lamps directly.

At the same time, many downstream companies have begun to package, and the packaging companies that are squeezed by both upstream and downstream can only go upstream or downstream. However, the investment scale and technical threshold of the upstream of the LED industry are much higher than those of the middle and lower reaches. The possibility of packaging companies expanding to the upstream is very small, so many packaging plants choose to expand downstream to make lamps.

As a result, packaging companies will move in two directions. The first is horizontal and vertical integration, taking the road of scale. The form and size of the package are made according to the needs of downstream customers. The demand of downstream customers leads to more models of packaged products, and such many product models do not meet the requirements of large production. Therefore, some packaging companies began to merge vertically and horizontally, and through large-scale production to ease the pressure of survival through joint and merger methods. Large enterprises form strategic alliances with the downstream and eat up the market space of small enterprises. This is the performance of centralized and large-scale market areas. Second, some packaging companies will extend downstream. Encapsulation-to-lighting companies can do their own packaging, then make products, and then use high-cost-effective and large-scale production to improve the competitiveness of enterprises, but the weakness of market channels is the biggest problem faced by these packaging plants.

Downstream: high-end and low-end products are clearly positioned

Most companies choose to do OEM or ODM for large domestic and foreign companies because of the high cost of capital for creating channels.

The most important feature of the global lighting market in 2013 is that with the rapid decline in the price of LED lighting products and the elimination of incandescent lamps, the global replacement of traditional light sources by LED light sources has exploded. Among them, bulbs and tubes are the most popular alternative sources. In 2014, reducing product prices, actively seeking bidding projects, vigorously building and transforming road lighting, promoting smart lighting and enhancing brand image will become the main development strategies of global LED lighting manufacturers.

As far as the domestic market is concerned, with the rapid start of the indoor lighting market, traditional lighting companies have gradually turned to the LED lighting market. Traditional lighting companies with rapid channel transformation have great advantages, but most LED companies will choose to OEM or ODM for domestic and foreign manufacturers because of the high capital cost of creating channels. Powerful LED companies are beginning to look for companies with channels and scale advantages to integrate or form strategic alliances.

Equipment: domestic MOCVD power storage

Equipment should not only have a large capacity, but also make the product consistency consistent, so that chip companies can accept domestic equipment.

The MOCVD epitaxial furnace is the core equipment for LED production. We generally use the number of MOCVD equipment as an indicator of productivity. By the end of 2012, there were 1,050 MOCVD equipment in China, and less than 500 units were actually mass-produced, and the operating rate was less than 50%. In the first half of 2013, the LED market was improving. LED companies continued to open MOCVD equipment that they had purchased, and gradually reached full-load production. The company is integrating through cooperation, mergers and acquisitions, and further releasing production capacity.

With the rapid development of the domestic chip industry, the localization rate of chips continues to increase, and the demand for equipment is gradually increasing. The domestic LED industry needs the emergence of a strong MOCVD equipment manufacturing enterprise belonging to its own country to enhance the technology and innovation capabilities of the entire LED industry. The success of domestic MOCVD equipment is mainly due to independent research and development and innovation. Domestic enterprises must understand the advantages and disadvantages of foreign equipment, and achieve technological breakthroughs in order to achieve localization in the true sense. After years of vigorous research and development and research on core technologies, many domestic enterprises have launched their own domestic MOCVD equipment, which also marks that Chinese enterprises have achieved certain results on the road of localization of core equipment for LED chip production. The localization of MOCVD equipment means that long-term foreign monopoly technology has been broken, and many domestic LED companies will bid farewell to the complete dependence on foreign equipment.

In 2014, domestic MOCVD equipment manufacturers will improve their own strengths in the following aspects: First, improve the consistency and stability of equipment, equipment should not only have large capacity, but also make product consistency, so that chip companies can accept Domestic equipment. The second is to increase the scale of production, and to accept large orders at home and abroad, and enterprises with industrial production capacity can achieve sustainable development. The third is to improve the technical support capabilities, communicate with the chip companies in a timely manner, and customize the equipment to meet the needs of customers. The fourth is to localize the core components. Parts processing involves gas control boxes, heaters, graphite trays, etc. It is very difficult to mature these parts. Therefore, many of the core components used by manufacturers producing MOCVD equipment are imported from abroad. In the long run, there is a lack of precision machining technology in China, and many parts require precision machining. Therefore, research on important key materials will also allow domestic companies to invest more energy. If we can break through these bottlenecks, domestic MOCVD manufacturers will certainly have a lot to do in the next few years.

New energy observation

Distributed photovoltaic "ride the horse"

Following the announcement by the National Energy Administration on November 18 last year of the “Notice on the Interim Measures for the Management of Distributed Photovoltaic Power Generation Projectsâ€, the development of distributed PV has once again ushered in significant material benefits. Recently, the “Notice on Promulgating the List of New Energy Demonstration Cities (Industrial Parks) (First Batch)†(hereinafter referred to as the “Noticeâ€) was released, and 81 cities and 8 industrial parks were among them.

Low-carbon economy, energy-saving and emission reduction have become the theme of the current era. Coupled with the increasingly prominent energy crisis, it is imperative to promote the development of new energy industry. The city is an important carrier of human activities and economic and social development, and also the region with the most concentrated energy consumption. The clean and efficient use of urban energy has a great impact on the sustainable development of cities. Thus, the concept of a new energy demonstration city came into being.

The so-called new energy demonstration city refers to a city that makes full use of the local rich renewable energy in urban energy development to make renewable energy reach a higher proportion or larger scale in energy consumption. The "Notice" requires that the construction of new energy demonstration cities should strengthen planning and coordination, integrate their construction into economic and social development plans and annual plans, and propose binding development indicators.

At the same time as the request is made, the National Energy Administration is also working hard to create conditions for the construction of new energy demonstration cities. The National Energy Administration not only conducts pilot projects for financial innovation in new energy demonstration cities by the United Nations Development Bank, but also encourages financial institutions to establish local investment and financing platforms to provide innovative financial services for the construction of new energy demonstration cities. It also stipulates that power grid enterprises should actively implement new energy demonstrations. The city's supporting power grid construction optimizes power system operation and provides system support for distributed generation applications and local consumption of renewable energy.

On the one hand, the central government's encouraging call, and on the other hand, the local government's positive response. In order to apply for the construction of a new energy demonstration city and finally obtain the title of a new energy demonstration city, it is first necessary to reach a hard target of the new energy alternative energy source and the proportion of urban energy consumption. In fact, although there are many new forms of energy available, such as solar thermal and biomass energy are unlikely to be the first choice. Because for the development of solar thermal, its implementation of solar water heaters has the characteristics of user dispersion and implementation difficulty; the development of biomass energy, the collection of burning materials such as straw is also a big problem. On the contrary, the use of new energy sources such as photovoltaics is relatively small and relatively easy to complete. At the same time, the advantage of solar photovoltaic power generation is distributed application, and distributed new energy power generation is just listed as one of the important development directions of the new energy demonstration city in the future. There is no doubt that the construction of new energy demonstration cities will open a new situation for promoting the development of China's distributed photovoltaic industry.

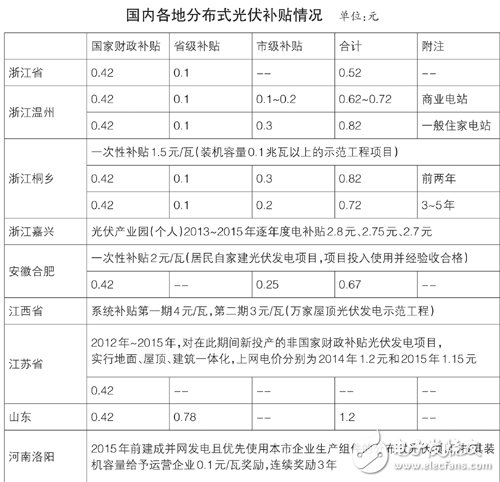

Based on this, a number of applicant cities have not only introduced a generous distribution of photovoltaic power subsidies, but also multi-party efforts to promote distributed photovoltaic applications. Take Hefei City, Anhui Province as an example, the distributed photovoltaic power subsidy is 0.25 yuan / watt, the residents will build a photovoltaic power generation project after the experience will receive a one-time subsidy of 2 yuan / watt, it is particularly worth mentioning that the city has a roof Photovoltaic power generation systems must be installed for non-residential civil, industrial, and municipal facilities with an area of ​​more than 1,000 square meters. Unlike the “recommendations†and “recommendations†of developing new energy sources in previous years, such “mandatory†policies highlight the city’s firm determination to follow the path of green sustainable development.

At the National Energy Work Conference held recently, in 2014, the domestic installed capacity of new PV was finalized to 14GW, of which distributed PV accounted for 60%, about 8GW. This goal has been criticized by some people as "too grand and unrealistic." At present, it seems that with the strong promotion of government departments at all levels, distributed photovoltaics have become more and more popular, and the seemingly unreachable targets have been getting closer and closer to us.

Extended reading

Lighting

SHENZHEN CHONDEKUAI TECHNOLOGY CO.LTD , https://www.szsiheyi.com